For the first time in venture history, three distinct channels share the liquidity burden roughly equally.

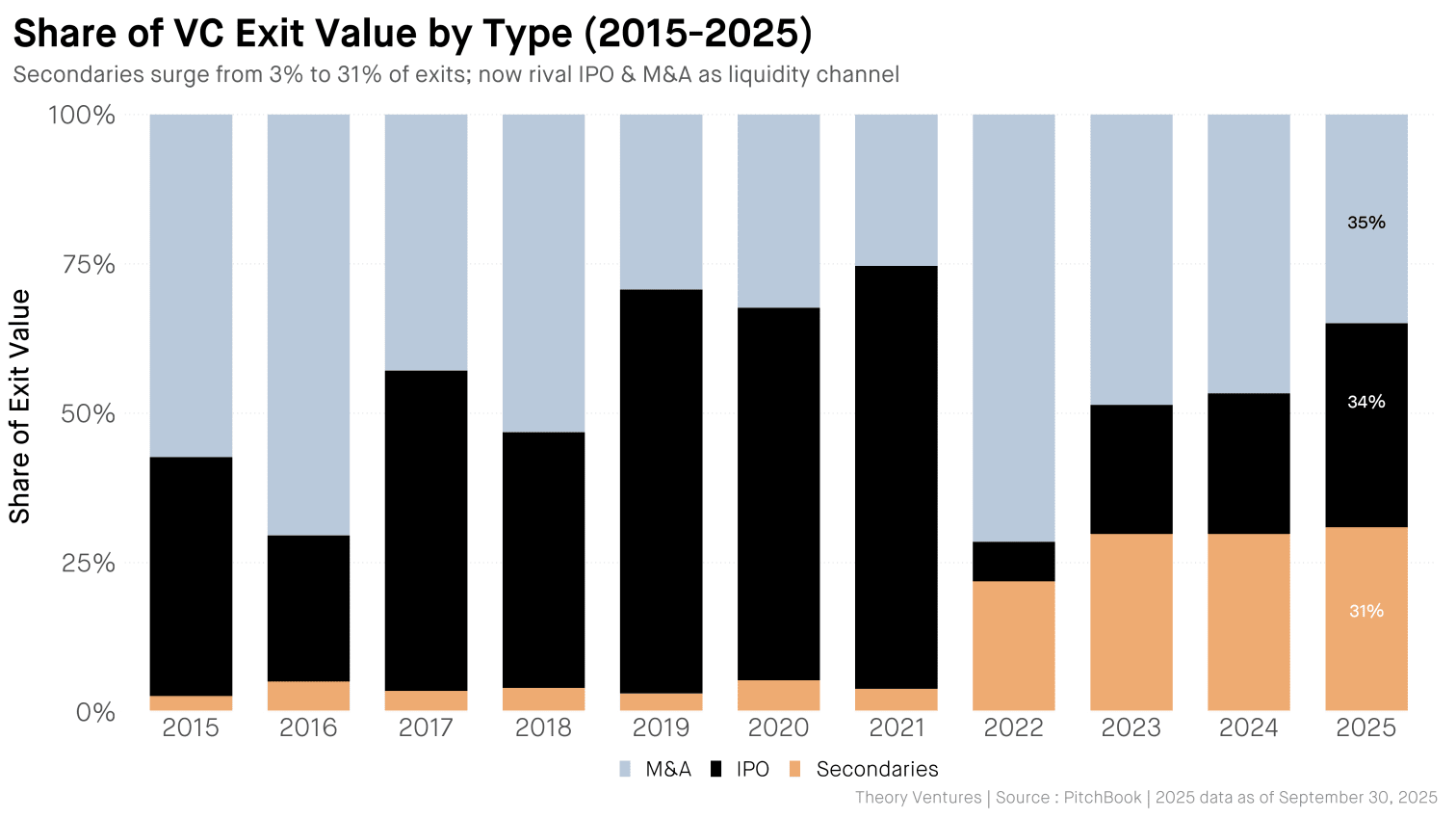

A decade ago, secondaries barely registered. They accounted for roughly 3% of exit value in 2015. Today they claim 31% : nearly $95b in the trailing twelve months.

The shift accelerated after 2021’s IPO bonanza. When public markets closed their doors in 2022, investors found alternative routes. Secondaries absorbed demand that would have flowed to traditional exits. When Goldman Sachs acquired Industry Ventures, the transaction signaled secondaries have arrived. Morgan Stanley followed with EquityZen, then Charles Schwab announced its acquisition of Forge Global. Wall Street recognized the structural change before most of venture did.

This matters for founders & investors. When IPOs dominated exits, fund models assumed a small number of public offerings would generate the bulk of returns.

Now liquidity arrives through multiple doors. A founder might sell secondary shares to patient capital while the company remains private. A GP might move positions through continuation vehicles. An LP might trade fund stakes on an increasingly liquid secondary market.

The 830 unicorns holding $3.9t in aggregate post-money valuation cannot all exit through IPOs. The math doesn’t work. At 2025’s pace of 48 VC-backed IPOs, clearing the unicorn backlog would take seventeen years. Secondaries provide a release valve that traditional exits cannot.

Companies like OpenAI have embraced this reality, running employee tender offers while voiding unauthorized secondary transfers. The largest private companies now manage their own liquidity programs rather than waiting for public markets.

Today, secondary liquidity concentrates in the top 20 names. SpaceX, Stripe, OpenAI. For the founder of company #50, the secondary market remains largely theoretical. For secondaries to succeed as a broad asset class, buyers must underwrite positions in companies without household recognition. As the market grows, this coverage gap becomes opportunity.

For LPs starved of distributions since 2022, the expansion of secondary channels offers hope. The $169b in cumulative negative net cash flows needs somewhere to go. More exit paths mean more opportunities to return capital.

When a Series B employee asks about liquidity today, the answer isn’t “wait for the IPO.” It’s “we’re planning a tender offer next year.”

A decade ago, secondaries were a footnote. Now they’re infrastructure. Liquidity flows where it can, not where tradition suggests it should.