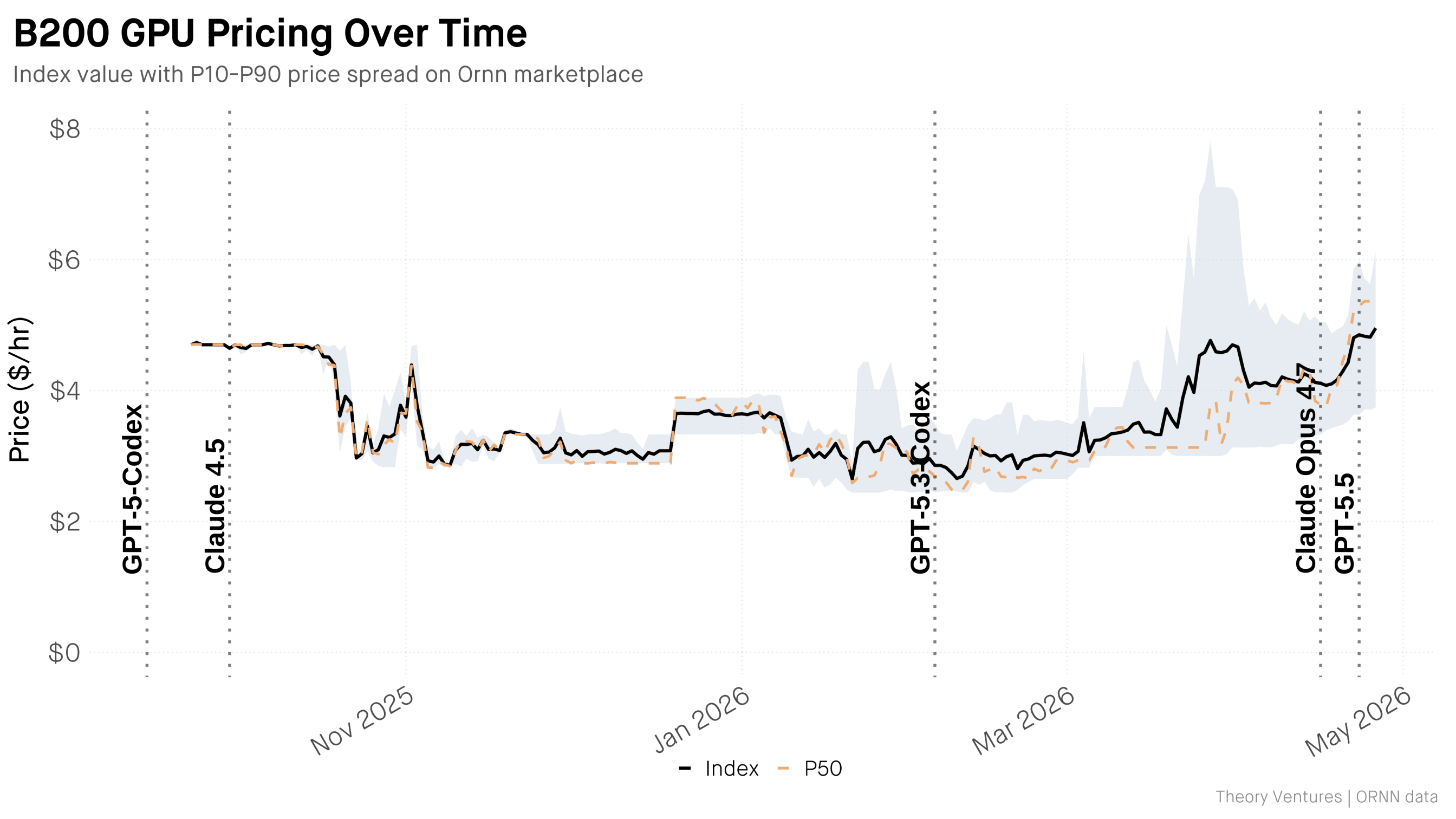

NVIDIA’s latest GPU rental prices on the Ornn Compute Price Index hit $4.95 per hour this week, up from $2.31 in early March : a 114% surge in six weeks.1

The price spread over prior-generation chips doubled from $0.28 to $1.80 per hour. The new chip is NVIDIA’s B200 (Blackwell); the prior generation is the H200 (Hopper).

The GPU market is becoming lucid - even if the fog hasn’t lifted.

1. Frontier model releases correlate with demand shocks

The price spikes line up with major model launches. Every major model release since September 2025 preceded or coincided with jumps in B200 pricing.

GPT-5.5’s expanded context window requires the memory headroom that only Blackwell provides.2

The correlation isn’t perfect. Supply shocks matter too. But the pattern is clear : newer models need newer chips.

2. The gap between cheapest & most expensive providers is blowing out

In September 2025, B200 prices across providers clustered tightly. Today the spread has more than doubled. Some providers still offer B200 at near-H200 prices. Others command scarcity premiums.

This bears the hallmarks of an opaque market with big supply/demand shocks. When is a hyperscaler receiving a new delivery? Which AI startup overbought capacity & is now selling at a discount? Opaque everywhere you look.

3. The B200-over-H200 price gap collapsed, then recovered

When B200 came to market in September 2025, it cost more per hour than H200. Buyers paid up for the extra memory & inference density.

By November, that gap collapsed to $0.28 as supply flooded the market. For a brief window, B200 & H200 reached near price parity.

Since February when GPT-5.3-Codex launched, the spread re-widened. The current $1.80 gap is back near launch levels.

The widening gap is also a depreciation signal : older chips lose value when new models demand new architectures.

For cloud providers, pricing power is returning. After six months of margin compression, the sellers’ market is back.

For AI startups, the spot market leads contract pricing by ~90 days. B200 likely settles above $5.00 for the summer.

For model builders, inference at the frontier is getting more expensive.

Inflationary demand outpaces deflationary algorithmic & chip improvements, but the fog of the GPU market continues.