Streaming is the next category to consolidate within the modern data stack. IBM announced its intent to acquire Confluent.

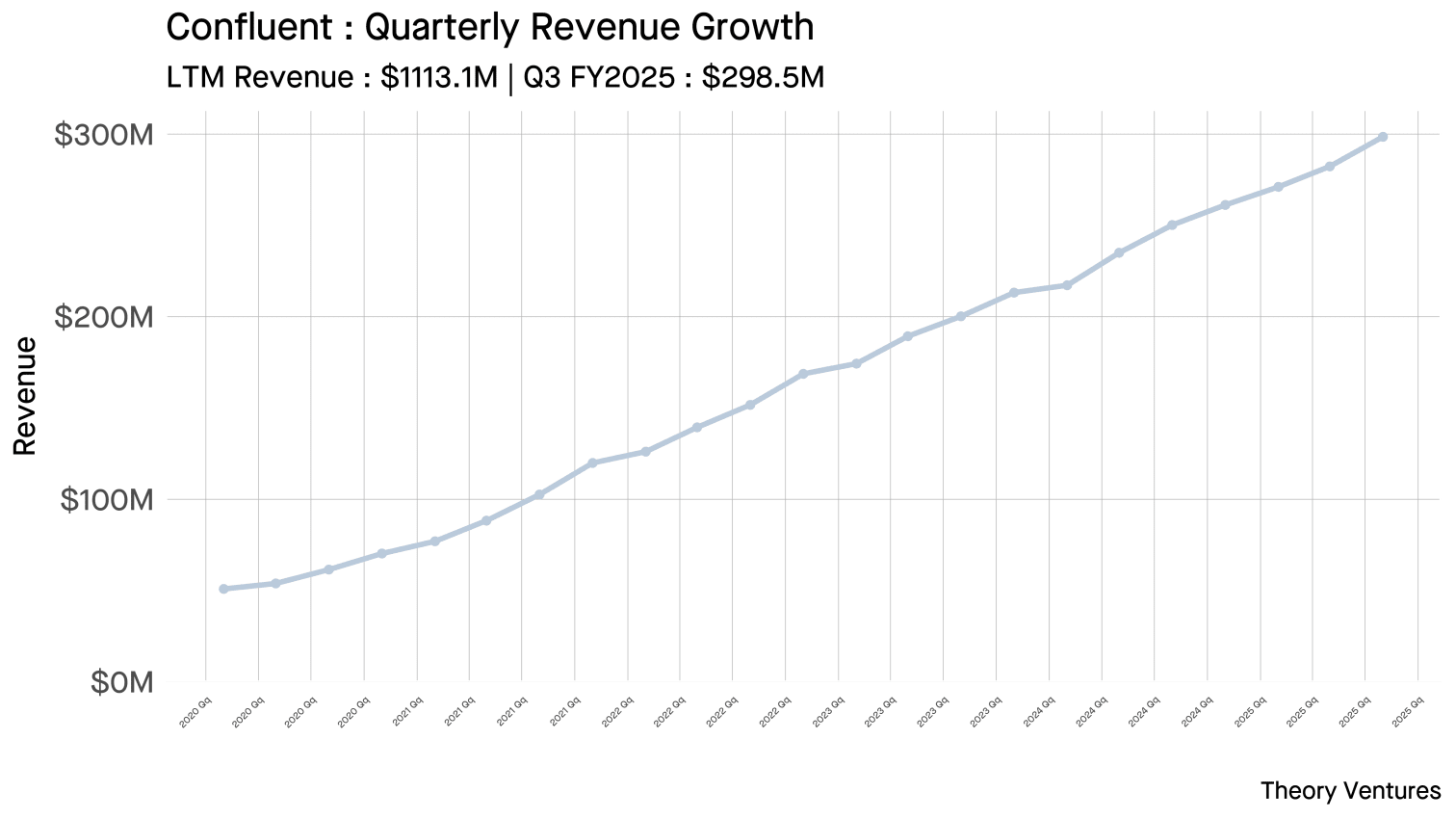

The deal values Confluent at $11.1 billion, or 10.0x LTM revenue. Confluent commands more than 40% of the Fortune 500 as customers & has grown into a $1.1 billion revenue business.

The founders of Confluent, including CEO Jay Kreps, created Apache Kafka, a streaming technology built inside LinkedIn. Founded in 2014, Apache Kafka now runs at more than 80% of the Fortune 100. Kafka powers real-time data pipelines & stream processing, updating data systems whenever a new event happens. When a taxi ride is booked, a credit card is swiped, or a user likes a comment, Kafka handles the data flow.

Confluent continues to grow nicely, with recent quarterly revenue of $298.5 million, growing 19.3% year over year. It has a gross margin of 74.1%, which is typical for software companies. Although its operating margins are negative, roughly -27%, this reflects a high cost of sales.

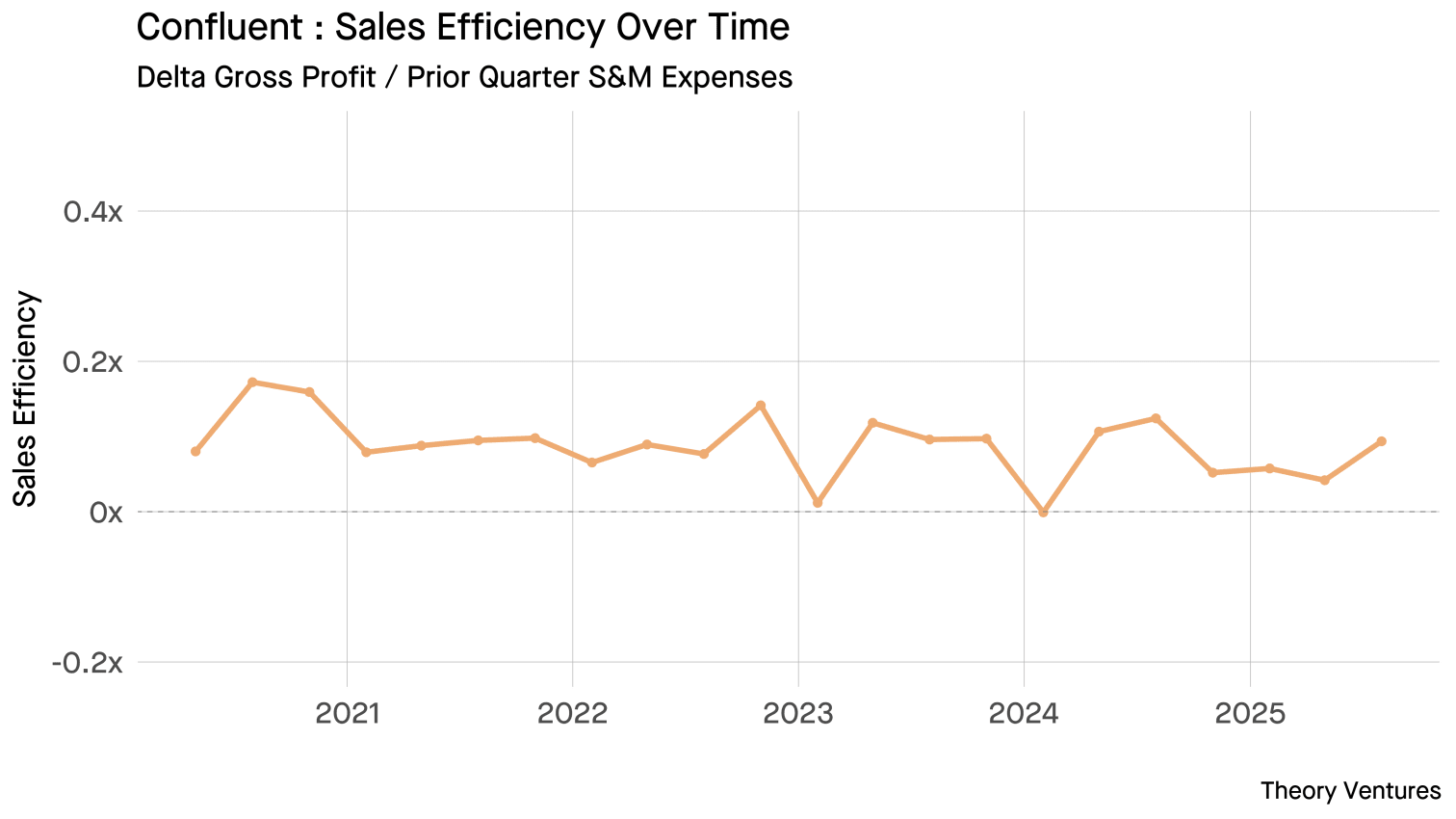

The company’s sales efficiency sits at 0.38x : Q3’s marginal gross profit of $13.5M annualized ($54M) divided by Q2’s selling & marketing expenses of $143.6M. For every dollar spent on S&M in one quarter, the company generates 38 cents in incremental gross profit the next quarter.

New customer acquisition reinforces the challenge.

| Price Point | Total Customers | Net New Q3 | % of Total |

|---|---|---|---|

| $20K+ ARR | 2,533 | +36 | 100% |

| $100K+ ARR | 1,487 | +48 | 59% |

| $1M+ ARR | 234 | +15 | 9% |

Confluent added 36 net new $20K+ customers in Q3. The $100K+ cohort represents the largest sequential increase in 2 years.

Growth comes primarily from expansion : net revenue retention sits at 114%, meaning existing customers increase spend by 14% annually. Gross retention hovers near 90%. The $100K+ customers account for more than 90% of ARR. Confluent’s challenge isn’t keeping customers. It’s acquiring new ones.

The most compelling trend : 10-percentage-point YoY improvement in operating margins, suggesting a path to profitability within 12-18 months.

Is Confluent a bargain or appropriately priced?

The bull case points to category-defining technology in Apache Kafka, 21%+ growth with improving margins, a clear path to profitability & critical infrastructure for AI & real-time applications. The bear case notes the company remains unprofitable, faces competitive threats from AWS Kinesis & Azure Event Hubs, competes with open-source Kafka alternatives & carries IBM integration execution risk.

| Company | Buyer / Market | Year | Revenue Growth | Revenue Multiple |

|---|---|---|---|---|

| Snowflake | Public | 2025 | 29% | 17.8x |

| MongoDB | Public | 2025 | 21% | 14.4x |

| Tableau | Salesforce | 2019 | 15% | 11.7x |

| Confluent | IBM | 2025 | 19% | 10.0x |

| Splunk | Cisco | 2023 | 16% | 5.3x |

A major question for Confluent over the last few quarters has been : what is the next adjacent product category to catapult another wave of growth? The AI surge has been a positive for the company.

Within IBM, Confluent may find its technology complementary to the raft of AI technologies demanded by large enterprises.