It’s not often that venture capital thinks about the credit markets. I remember becoming a venture capitalist three months before Lehman fell, when mortgage securities topped the news of the global financial crisis.

Recently Oracle’s bonds have been weighing on my mind.

AI’s capital expenditure in 2025 represents about 1.6% of US GDP. In 2026, that number should top 3% of US GDP according to Goldman Sachs estimates1.

Google, Microsoft & Amazon do not have the capital necessary on their balance sheets to fund this buildout without debt.

So, they have been issuing bonds. Oracle is no different, aside from operating at a much smaller scale with a far smaller bank account & a bigger proverbial mortgage.

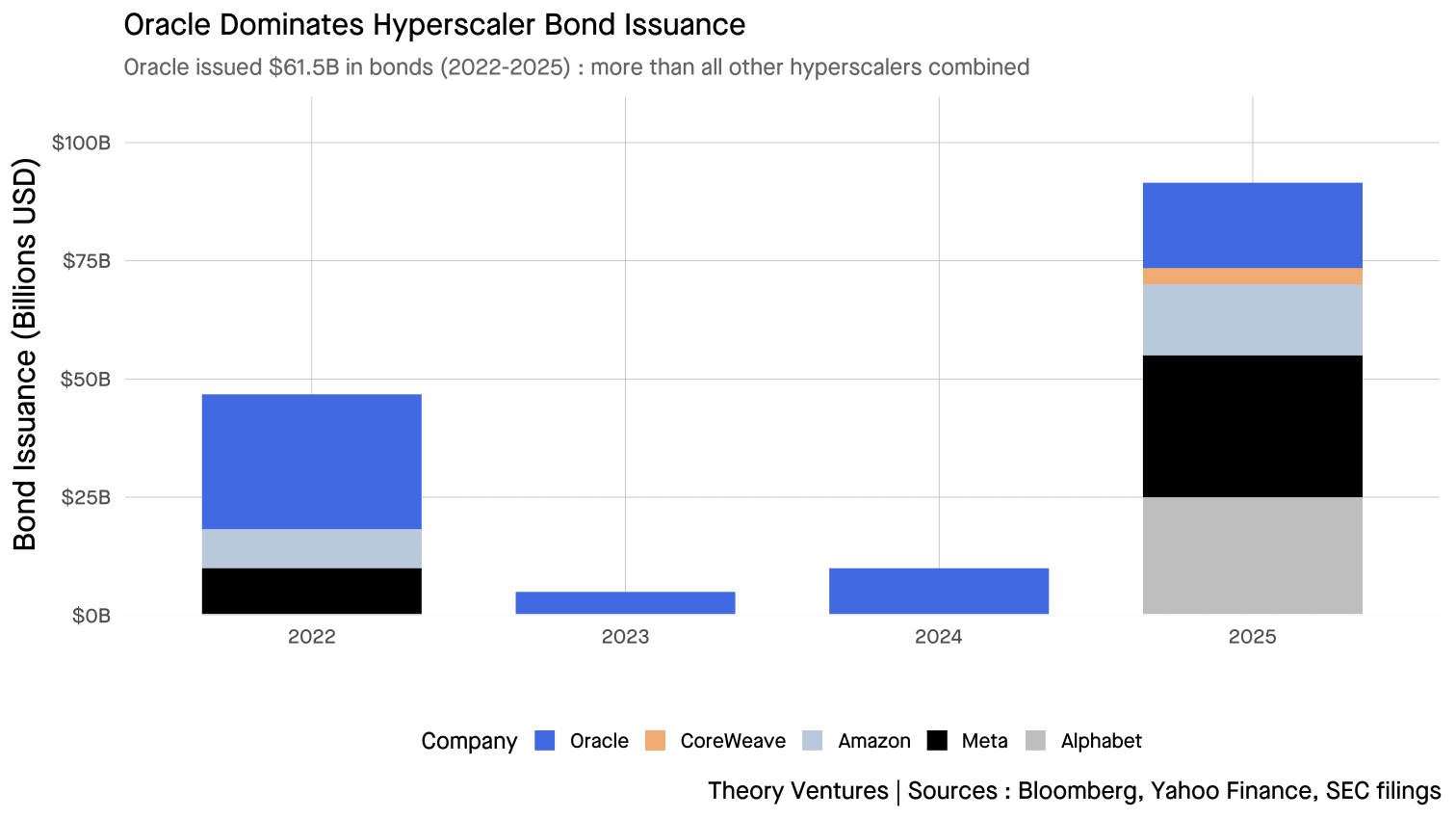

In 2025 alone, hyperscalers issued $121 billion in bonds, more than four times the five-year average of $28 billion2. Oracle led with $61.5 billion total across 2022-2025, driven by its $28.5 billion Cerner acquisition financing & $18 billion AI infrastructure raise. Meta’s $30 billion October offering was the largest corporate bond sale since 2023, while Alphabet raised $25 billion in November. Microsoft remains the only hyperscaler not tapping debt markets recently.

The Initial Euphoria & Subsequent Reality

For Oracle, the initial euphoria following the OpenAI deal bathed the company in bullish sentiment. The $300 billion partnership with OpenAI was hailed as Oracle’s ticket to the AI infrastructure big leagues3.

Despite record-breaking remaining performance obligation (RPO) growth of 438% to $523 billion, actual revenue has not increased as quickly as hoped.

More telling, however, are the credit default swaps.

The Credit Market’s Response

In November 2025, Barclays downgraded Oracle’s debt to underweight, warning it could fall to BBB-, the lowest investment-grade rating before junk status4. In December, the situation deteriorated sharply after Oracle’s earnings report revealed capital expenditures of $12 billion in Q2 (versus $8.25 billion expected), with FY 2026 CapEx guidance raised by $15 billion to a total of $50 billion5.

The bond market’s reaction was swift & bracing. Oracle’s credit default swap spreads widened to above 125 basis points, levels not seen since the 2009 financial crisis6. Despite maintaining official ratings of Baa2 (Moody’s) & BBB (S&P), Oracle’s bonds now trade like junk bonds in the secondary market.

The Leverage Problem

Oracle’s debt-to-equity ratio has ballooned to 500%, dwarfing its cloud computing peers.

Why is Oracle’s debt-to-equity ratio so much higher?

-

Small equity base : Oracle operates with just $20B in shareholders’ equity compared to $340B+ for Microsoft & Google7. This is the denominator problem : even moderate debt levels become astronomical ratios when divided by such a small equity base.

-

Absolute debt comparable to giants : Oracle’s $100B total debt actually exceeds Microsoft ($80B) & Amazon ($65B), but those companies have 4-17x more equity to support it7. Oracle is borrowing like a hyperscaler without the balance sheet of one.

-

Rapid equity erosion : The $50B FY 2026 capital expenditure guidance5 is burning through Oracle’s equity cushion. With negative $10B free cash flow in Q2 alone, equity shrinks with each quarter of aggressive buildout.

-

Revenue scale mismatch : Oracle generated $16.06B in Q2 revenue5, putting it on pace for ~$64B annually, versus $200B+ for Microsoft & Amazon. The company is taking on debt loads designed for businesses 3-4x larger.

-

Legacy business constraints : Oracle’s mature database & enterprise software business generates steady cash but minimal equity growth. Unlike the hyperscalers’ high-margin cloud businesses that compound equity rapidly, Oracle’s core business can’t offset the AI infrastructure cash burn.

| Company | Total Debt | Total Equity | Debt-to-Equity Ratio | Credit Rating |

|---|---|---|---|---|

| Oracle | $100B | $20B | 500% | Baa2/BBB (negative outlook) |

| CoreWeave | $6B | $5B | 120% | Not rated |

| Amazon | $65B | $286B | 23% | AA- |

| Microsoft | $80B | $343B | 23% | AAA |

| $27B | $387B | 7% | AA+ | |

| Meta | $29B | $194B | 15% | AA- |

Sources : Company 10-K & 10-Q filings (Q3-Q4 2024), Oracle Q2 FY 2026 earnings, Yahoo Finance, Simply Wall St

Oracle’s leverage is 20+ times higher than Microsoft & Google, despite generating only a fraction of their revenue. The company carries $100 billion in total debt while operating at a fundamentally different scale than the hyperscalers it’s trying to compete against.

The Concentration Risk

Projected customer concentration with OpenAI could represent 33% of Oracle’s revenue by 2028. As Barclays analysts noted, if OpenAI were to experience financial difficulties or choose to diversify its infrastructure partners, Oracle would face an immediate & severe revenue shortfall with few alternatives to backfill that capacity.

How Could Oracle Achieve Their Goal?

Oracle’s management has attempted to assuage investor concerns by arguing they will need “substantially less” than the $100 billion market analysts estimate for their AI buildout. They cite innovative financing models :

- Customer-supplied chips : Customers bring their own GPUs (zero CapEx for Oracle)

- Vendor chip rentals : Suppliers rent chips instead of selling them

- Late-stage equipment purchases : Buying hardware “very late in production cycle”

- No upfront data center costs : Zero expense until facilities are operational

Barclays predicts Oracle may run out of cash by November 2026 if the current trajectory continues4. Starting FY 2027 (June 2026), Oracle faces financing gaps that will require either additional debt issuance at punitive rates or a fundamental slowdown in the AI buildout.

The Financial Engineering Alternative : Off-Balance-Sheet AI Infrastructure

While Oracle loads debt onto its balance sheet, other hyperscalers have found a different path : off-balance-sheet financing through infrastructure partnerships.

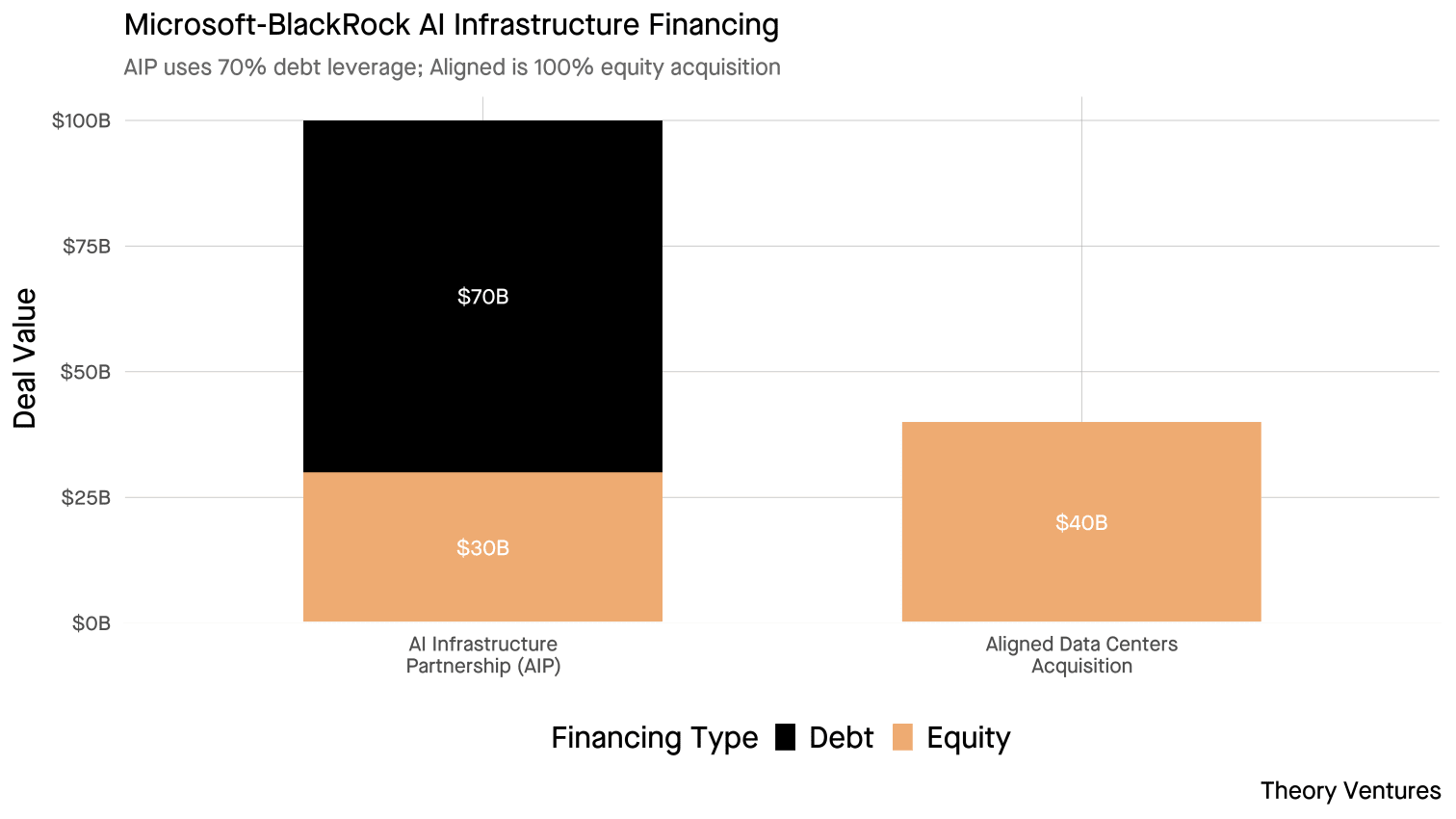

Microsoft-BlackRock AI Infrastructure Partnership (AIP)

In September 2024, BlackRock, Global Infrastructure Partners (GIP), Microsoft, & MGX launched the AI Infrastructure Partnership with a distinctive financing structure8.

The partnership’s first major deployment : the $40 billion acquisition of Aligned Data Centers in October 2025, the largest data center deal ever9. But it’s not the only one. Private equity has been extremely acquisitive with data center acquisitions, often funding these purchases with a majority of debt.

With this deal, BlackRock GIP + Microsoft now matches Blackstone as the largest data center acquirer, each with ~$40B in total deal value since 2021.

Why this structure matters : The 70% debt leverage sits at the fund level, not on Microsoft’s corporate balance sheet. Microsoft contributes equity to the partnership, gets AI infrastructure exposure, but the debt doesn’t appear in Microsoft’s 10-K. This is why Microsoft remains “the only hyperscaler not tapping debt markets recently” for direct corporate bond issuance.

Meta-Blue Owl Hyperion Joint Venture

Meta took this even further in October 2025 with Blue Owl Capital :

| Component | Amount | Notes |

|---|---|---|

| SPV Debt (A+ rated) | $27B | Anchored by PIMCO ($18B), BlackRock ($3B) |

| SPV Equity | $2.5B | Blue Owl contribution |

| Total Financing | ~$30B | Largest private credit transaction ever |

| Meta Ownership | 20% | Blue Owl owns 80% |

| Meta Cash Received | $3B | One-time payout at close |

Meta gets to lease back the completed 4-million-square-foot Hyperion data center, the company’s largest AI-optimized facility, while keeping the $27B debt off its balance sheet entirely10.

The Balance Sheet Arbitrage

Oracle, Microsoft, & Meta employ fundamentally different approaches to financing AI infrastructure. Oracle loads debt directly onto its corporate balance sheet, pushing its debt-to-equity ratio to 500% & threatening its credit rating. Meanwhile :

- Microsoft participates in $100B of AI infrastructure through AIP with essentially zero additional corporate debt

- Meta finances $30B of AI infrastructure through Blue Owl with zero corporate debt, while receiving $3B in cash

- The AIP fund operates at 233% leverage, but that’s the fund’s problem, not Microsoft’s

The Borrowing Aphorism

There’s an old saying about borrowing. If I owe you one dollar, that’s my problem. If I owe you a billion dollars, that’s your problem.

With hundreds of billions in debt financing AI infrastructure, and Oracle alone carrying $100 billion while its bonds trade like junk, that aphorism echoes in the background.

Addendum : A Better Way to Measure Leverage

Thanks to reader Alexander S. who suggested this.

The debt-to-equity ratios above are directionally correct but potentially misleading. Oracle’s book value (equity) is depressed by decades of stock repurchases & dividends. This shrinks the denominator, inflating the ratio. Most of the S&P 500 would appear significantly overleveraged when evaluated this way.

The better approach : Measure leverage as a multiple of earnings. Debt/Operating Income shows how many years of operating profit would be required to retire all debt.

| Company | Total Debt | Operating Income | Debt/OpInc | Years to Payback |

|---|---|---|---|---|

| Oracle | $131.7B | $17.7B | 7.4x | 7.4 years |

| Microsoft | $43.2B | $128.5B | 0.3x | 4 months |

| Apple | $90.7B | $133.1B | 0.7x | 8 months |

| Amazon | $62.2B | $68.6B | 0.9x | 11 months |

| Alphabet | $23.6B | $112.4B | 0.2x | 2.5 months |

| Meta | $28.8B | $69.4B | 0.4x | 5 months |

The hyperscalers could pay off all debt in under one year of operating income. Oracle would need 7.4 years at current levels. Investment grade thresholds typically sit at 2.5-3.5x.

This earnings-based view better explains why bond markets price Oracle debt like junk : it’s not the absolute debt level, but the debt relative to Oracle’s capacity to service it through operations.

References

Additional Data Sources : Moody’s Investors Service, S&P Global Ratings, CoreWeave company estimates (2024), Microsoft News on GAIIP Partnership (September 2024).

-

Goldman Sachs Global Investment Research, “AI Infrastructure Capital Expenditure Outlook 2025-2026” (November 2024) ↩︎

-

Bank of America Equity Research, “Hyperscaler Bond Spreads Widen as Tech Giants Issue Record Debt” (November 2025). Investing.com ↩︎

-

Oracle Press Release, “Oracle & OpenAI Expand Partnership with $300 Billion Multi-Cloud Agreement” (September 2025) ↩︎

-

Barclays Equity Research, “Oracle Corporation : Downgrade to Underweight on Leverage Concerns” (November 2025) ↩︎ ↩︎

-

Oracle Corporation Q2 Fiscal Year 2026 Earnings Call Transcript (December 9, 2025) ↩︎ ↩︎ ↩︎

-

Bloomberg Terminal, Oracle 5-Year Credit Default Swap Data (accessed December 14, 2025) ↩︎

-

Company Financial Statements : Microsoft 10-K FY2024 (filed July 2024), Amazon 10-Q Q3 2024 (filed September 2024), Meta 10-Q Q3 2024 (filed September 2024), Alphabet 10-Q Q3 2024 (filed September 2024), Oracle 10-Q Q2 FY2026 (filed November 2025). Equity calculations : Total Shareholders’ Equity from consolidated balance sheets; Debt-to-Equity ratios calculated as Total Debt ÷ Total Equity × 100. ↩︎ ↩︎

-

Microsoft News, “BlackRock, Global Infrastructure Partners, Microsoft, & MGX Launch AI Infrastructure Investment Partnership” (September 2024). Microsoft News ↩︎

-

BlackRock Press Release, “AI Infrastructure Partnership Acquires Aligned Data Centers for $40 Billion” (October 2025). CNBC ↩︎

-

Meta Investor Relations, “Meta Announces Joint Venture with Funds Managed by Blue Owl Capital to Develop Hyperion Data Center” (October 2025). Meta Newsroom ↩︎