After writing about the SpaceX, OpenAI & Anthropic IPO liquidity problem, readers asked : what about Saudi Aramco? At $29.4b raised & a $1.7t market cap, it’s the largest IPO in history. Doesn’t it prove mega-IPOs can work?

Aramco isn’t a good proxy. The next biggest example, Alibaba at $231b, is a better parallel.

| Company | IPO Year | Market Cap at IPO | Market Cap Now | Float at IPO | Float Now |

|---|---|---|---|---|---|

| Saudi Aramco | 2019 | $1.7t | $1.66t | 1.5% | 2.4% |

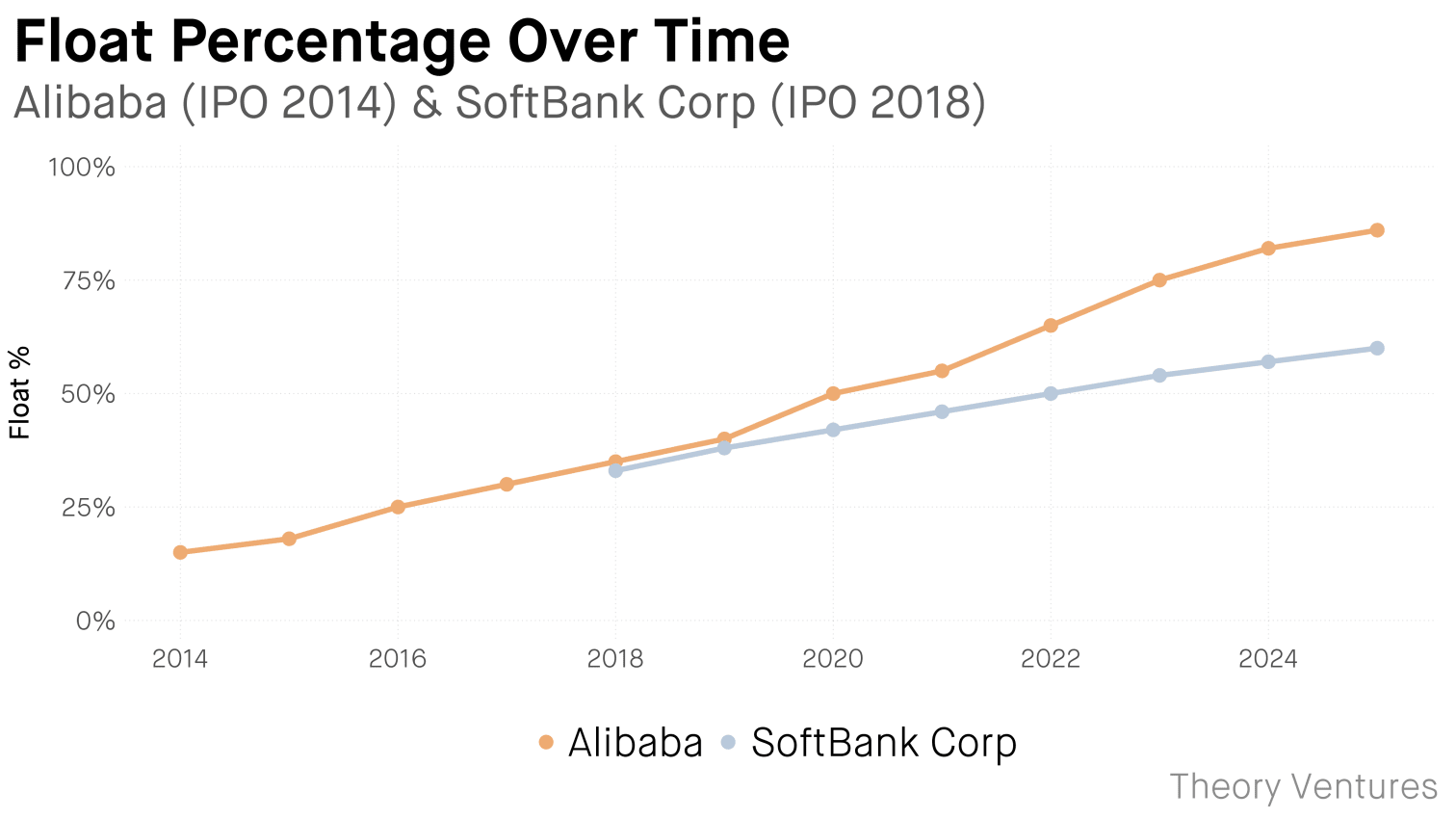

| Alibaba | 2014 | $231b | $365b | 15% | 86% |

| SoftBank Corp | 2018 | $70b | $66b | 33% | 60% |

In 2019, Aramco floated 1.5% of the company. Six years later, it’s still just 2.4%. The Saudi government holds 81% directly; the sovereign wealth fund holds another 16%. The IPO served strategic goals beyond capital markets.

Contrast Alibaba & SoftBank. Both started with real floats & expanded as founders & early investors exited. Alibaba’s float grew from 15% to 86%. SoftBank’s nearly doubled.

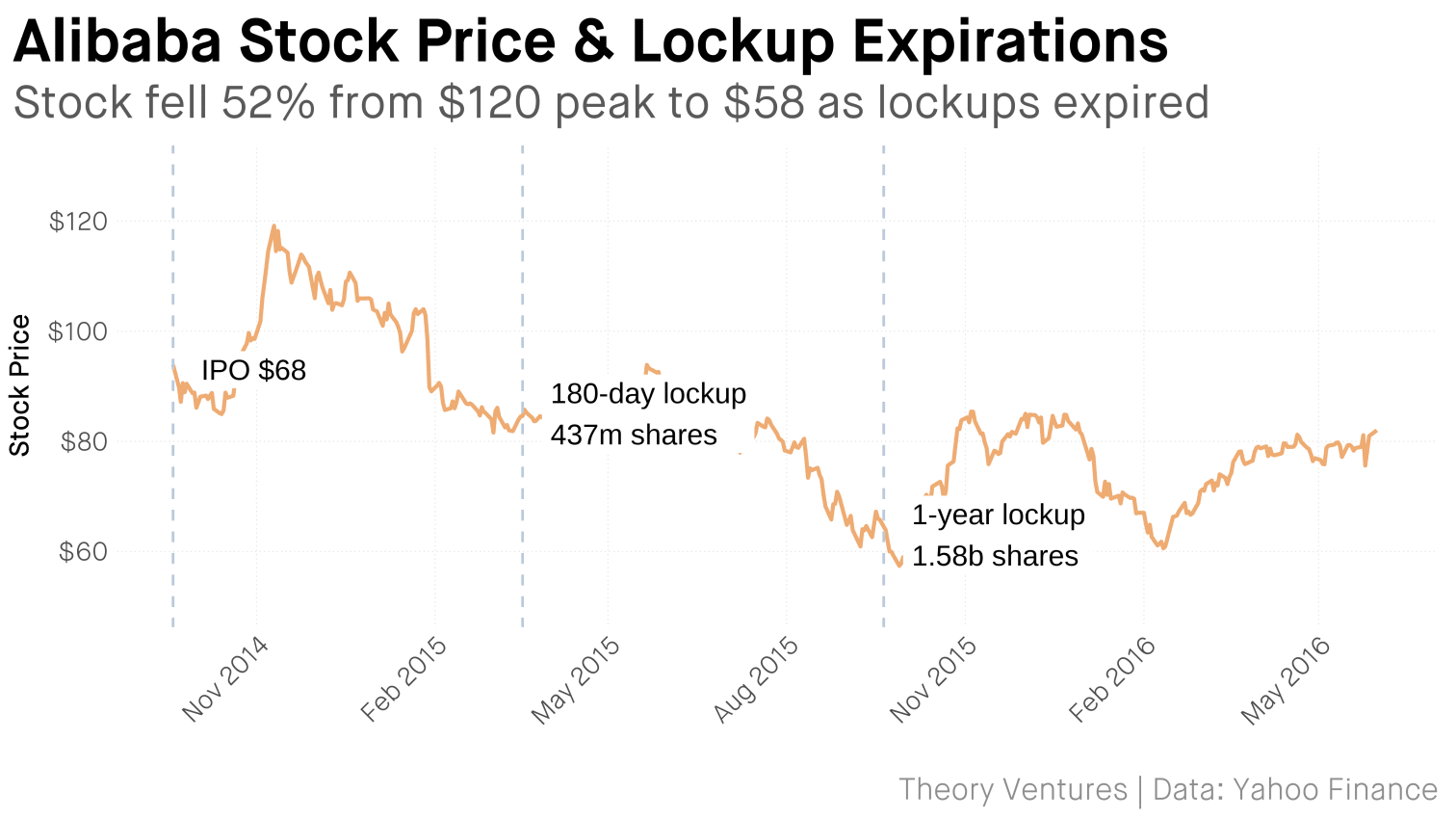

Float expansion is only half the story. The other half is timing. When do those shares actually hit the market? The typical IPO has a 180-day lockup, a period when insiders cannot sell shares.

The September 2015 unlock released 5x more shares than the IPO itself. The stock fell 52% from its $120 peak to $58, below the IPO price.

SpaceX, OpenAI & Anthropic may face less pressure. All three have run regular tender offers for years, allowing employees & early investors to sell before any IPO. SpaceX runs tenders 2-3x per year. OpenAI completed a $10.3b secondary sale in 2025. Anthropic launched its first tender in early 2025 at $350b. Much of the pent-up selling has already occurred.

But even Alibaba at $231b was a fifth to a tenth the size of SpaceX’s target. The market has never absorbed a trillion-dollar IPO where liquidity was the goal.