Motive, the AI-powered fleet management company formerly known as KeepTruckin, filed their S-1.

Founded in 2013 by Shoaib Makani, Ryan Johns, & Obaid Khan, the company has grown from an electronic logging device (ELD)1 compliance tool into a comprehensive physical operations platform serving nearly 100,000 customers across trucking, construction, oil & gas, & manufacturing.

Motive’s platform has since expanded beyond compliance to combine AI-powered dashcams for driver safety, GPS tracking for real-time visibility, & spend management cards to control costs. This suite acts as a central operating system for physical economy businesses, unifying data from vehicles, drivers, & equipment into a single interface.

| Metric | Motive (2025) | Samsara (at IPO) |

|---|---|---|

| ARR | $501M | $492M |

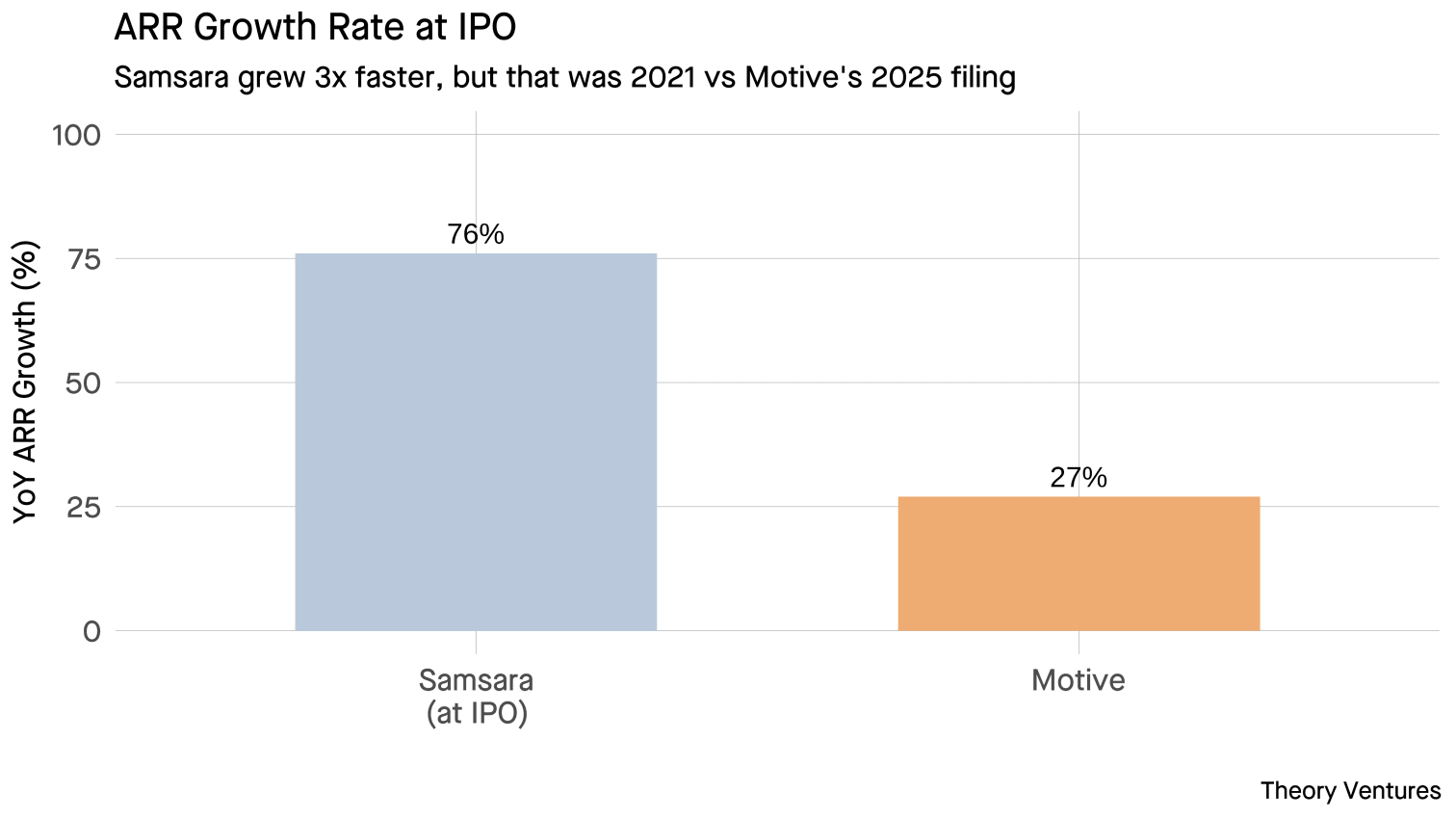

| ARR Growth | 27% | 76% |

| Gross Margin | 70% | 70% |

| Core Customers (>$7.5k / >$5k) | 9,201 | 13,000+ |

| Large Customers (>$100k) | 494 | 715 |

| Core NDR | 110% | 115% |

| Large NDR | 126% | >125% |

| Net Income Margin | -42% | -34% |

| Employees | 4,508 | ~1,500 |

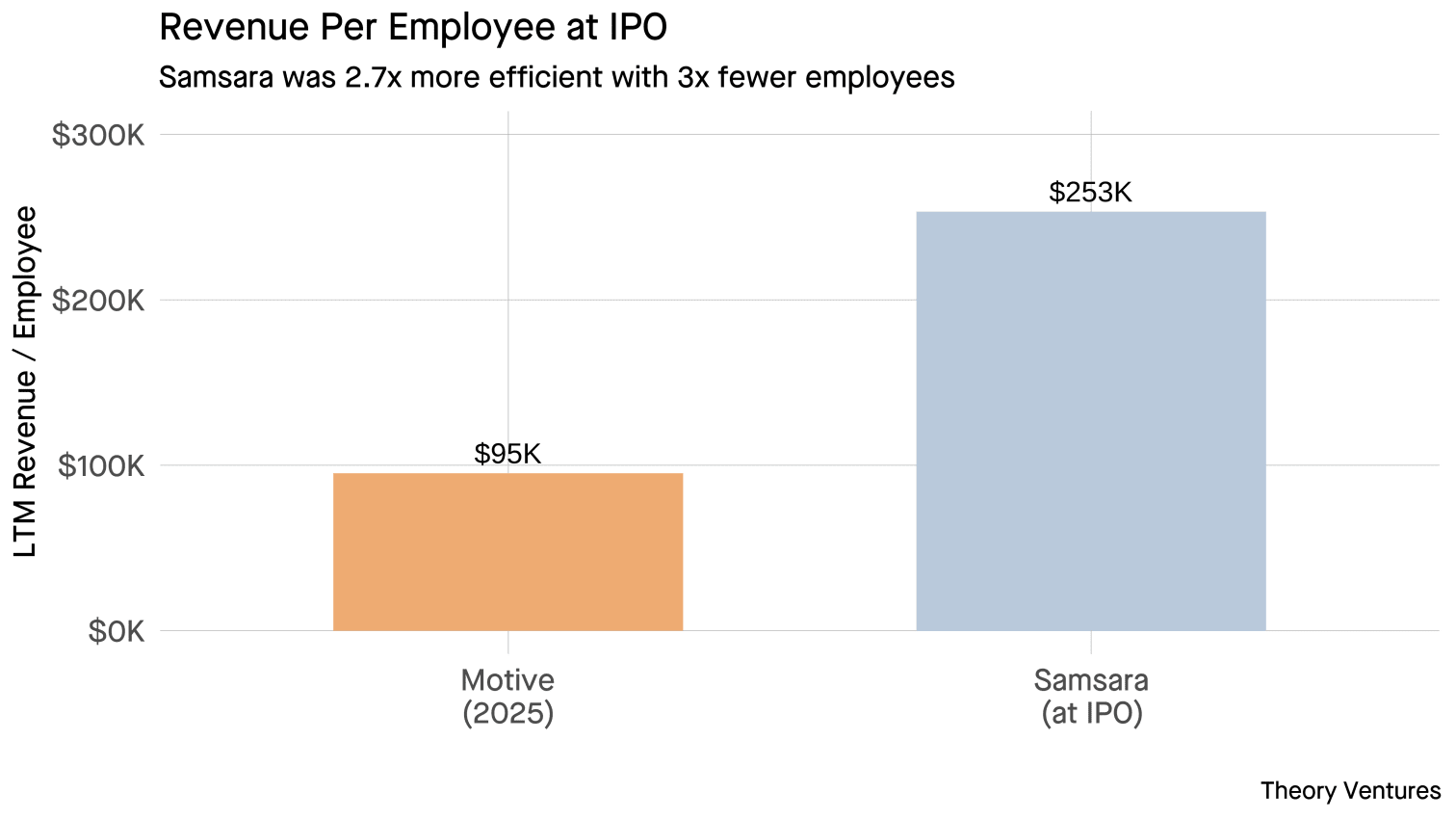

| ARR / Employee | $111k | $328k |

| ACV (Large >$100k)2 | $375k | $303k |

| ACV (Total) | $5k | $17k |

| Equity Raised | $600M | $930M |

Both companies achieved roughly $500m in ARR at the time of IPO.

Samsara grew 76% annually at IPO compared to Motive’s 27%. This growth was fueled by higher sales efficiency, likely driven by deal size; Samsara’s average contract value (ACV) of $17k was more than three times Motive’s $5k.

This disparity likely stems from different initial go-to-market strategies. Motive initially focused on the SMB segment (specifically owner-operators & small fleets needing a cost-effective compliance solution for the ELD mandate), building a massive base of smaller customers.

Motive’s ACV of $5k closely mirrors Fleetmatics’3 ACV of $6.8k at its IPO, confirming Motive joined Fleetmatics as a high-volume SMB player, but with modern AI capabilities. In contrast, Samsara targeted mid-market industrial operations from the start.

While legacy players like Geotab & Verizon Connect (Fleetmatics) maintain large installed bases, Samsara & Motive are capturing share with modern, AI-first platforms.

| Company | Revenue / ARR | Connected Assets | Status |

|---|---|---|---|

| Geotab | $1B (Est) | 5M+ | Market Share Leader |

| Samsara | $1.52B (LTM) | 2M+ | Revenue Leader |

| Verizon Connect | $600M+ (Est) | 2M+ | Incumbent |

| Motive | $501M (ARR) | 500k+ | Challenger |

Motive’s customer metrics reveal an enterprise-focused growth strategy. Large customers (>$100k ARR) grew 58% year-over-year, from 312 to 494. This 58% growth in large accounts compares favorably to Samsara, which grew its $100k+ customer count 48% year-over-year at the time of its IPO.

Motive’s enterprise accounts grow at 126% net dollar retention, meaning the average large customer spends 26% more each year. The company is successfully landing & expanding within enterprise accounts.

Core customers grew at 17%, from 7,875 to 9,201.

Both companies maintain similar 70% gross margins, impressive for businesses that ship hardware with their software. This positions them at the median for public SaaS companies, despite the hardware component.

The profitability picture differs. Motive’s net loss margin expanded from -35% in 2023 to -42% in the most recent period, while Samsara improved from -100% to -34% in the nine months before its IPO. Samsara’s improvement was driven by operating leverage : revenue grew 108% while sales & marketing expenses increased 11%.

Despite similar gross margins, Motive’s bottom line is weighed down by significantly higher “Other Expense” ($57M in the last nine months). This figure includes $22M in interest expense on approximately $300M of term debt, with the remainder driven by non-cash charges related to convertible securities.

Samsara generated $328k in ARR per employee at IPO. Motive generates $111k, roughly one-third. With 4,508 employees versus Samsara’s 1,500 at IPO, Motive has built a much larger organization to achieve similar scale, with about 3.2k employees in Pakistan.

Samsara trades at approximately 14x forward revenue, roughly in line with other vertical SaaS companies.

Motive has raised $600 million from Kleiner Perkins, GV, BlackRock, & others at a $2.85 billion valuation. With $500M in ARR, that implies a roughly 6x ARR multiple in the private markets.

Despite Motive having raised approximately $600 million in equity capital, Samsara’s path to IPO was significantly more capital-intensive, with over $930 million raised pre-IPO. However, Motive’s reliance on debt, holding roughly $300 million in term loans, partially offsets this difference in total capitalization, highlighting contrasting financing strategies between the two leaders.

Given these factors, what is Motive worth? Using an interaction model4, which is a refinement on the initial linear model, the analysis implies a valuation of approximately $3.7 billion.

Congratulations to the Motive team on reaching this milestone. Building a $500M ARR business in physical operations is no small feat, especially in a competitive market.

-

An ELD is a hardware sensor that connects to a vehicle’s engine to track driving hours, a requirement mandated by federal law for safety. ↩︎

-

ACV for Large Customers is calculated by dividing the ARR segment share (37% for Motive, 44% for Samsara) by the reported large customer counts (494 & 715, respectively) as disclosed in the filings. All other figures are pulled directly from the S-1 & IPO prospectuses. ↩︎

-

Verizon acquired Fleetmatics in 2016 for $2.4 billion in cash, representing a roughly 7.0x forward revenue multiple. ↩︎

-

Updated on Dec 30, 2025. The valuation model uses an Interaction Model (Growth × Margin) which improved statistical fit (R-squared 0.35 → 0.41). The model assumes a 27% forward growth rate (consistent with reported ARR growth) and a -42% net income margin. For comparison, the most recent nine-month historical GAAP results show 21.7% revenue growth and a -42.3% net income margin. The final valuation is derived by applying the predicted multiple to Motive’s estimated NTM revenue (Current ARR × (1 + Growth/2)). ↩︎