AI companies have committed $9.75b in 12 months to forward-deployed engineering. The FDE model, embedding engineers inside customers to deploy AI, has gone from a Palantir signature to an industry default.

That commitment is one quarter of Accenture’s annual labor cost.1

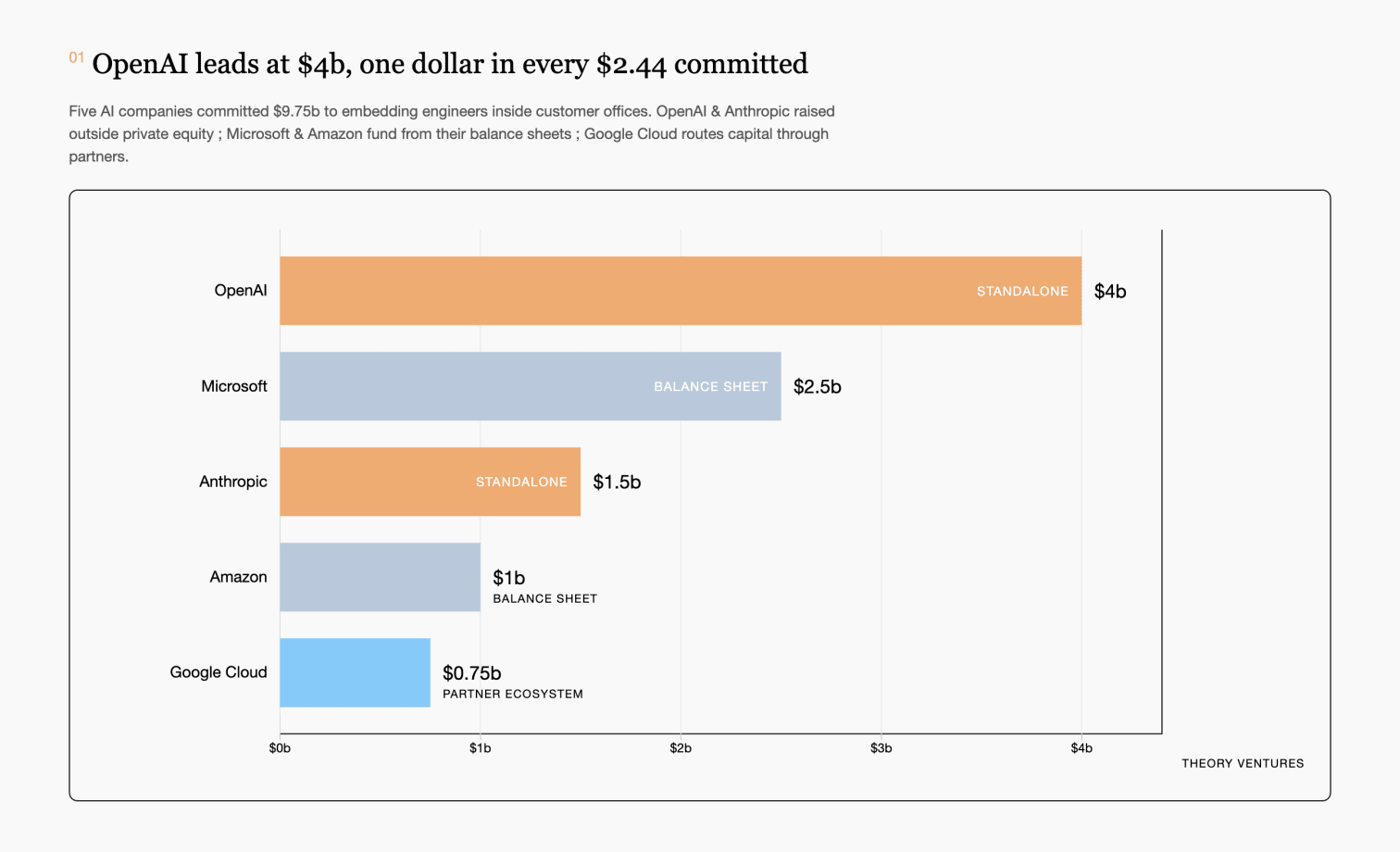

Three structural models are emerging.

The Balance Sheet. Microsoft & Amazon fund FDE teams from existing headcount. No external capital. Speed & control : Microsoft can reassign engineers without board approval. Salesforce, for example, has committed 1,000 FDE roles.2

The Standalone. OpenAI & Anthropic created standalone entities with external private equity. OpenAI’s Deployment Company raised $4b at a $14b post-money valuation with a 17.5% return floor.3 Anthropic raised $1.5b from Blackstone ($300m), Hellman & Friedman ($300m), Goldman Sachs ($150m), & others.4 Scale without diluting the parent. OpenAI acquired Tomoro, a 150-person Edinburgh consultancy with clients including Virgin Atlantic, Tesco, & the NBA.3 Anthropic targets Blackstone’s 275 portfolio companies first.4

The Partner Ecosystem. Google Cloud committed $750m to a partner fund rather than building direct.5 Capital flows to system integrators & specialists who deploy Google’s models. Leverage : one dollar mobilizes many dollars of partner headcount.

Why now? The bottleneck shifted from model capability to deployment. GPT-4, Claude, & Gemini are powerful enough. Most enterprises cannot install, configure, & operate them without embedded engineering.

FDE investment is a moat. Education builds trust : embedded engineers teach the customer how to use AI. Once a team is trained on one lab’s patterns, retraining on a competitor’s stack is friction no manager volunteers for.

They also see proprietary workflows, data schemas, & failure modes no API call reveals, & that intelligence flows back into model tuning. They expand across the organization, & when a competitor knocks, the embedded team is the defense.

The switching cost is institutional, not technical. And there’s $10b behind it.

-

Accenture FY2025 cost of services : $47.45b, 68.1% of $69.67b revenue. $9.75b / $47.45b = 21%. Accenture ↩︎

-

Salesforce : 1,000 FDE roles committed. Salesforce ↩︎

-

OpenAI Deployment Company : $4b raise at $14b post-money, 19 investors led by TPG, 17.5% return floor. Tomoro acquisition : Edinburgh-based FDE consultancy founded 2023, 150 employees, clients including Virgin Atlantic, Supercell, Tesco, Fidelity International, Red Bull, Mattel, NBA. OpenAI ↩︎ ↩︎

-

Anthropic standalone entity : $1.5b from Blackstone ($300m), Hellman & Friedman ($300m), Goldman Sachs ($150m), Apollo, General Atlantic. Blackstone has 275 portfolio companies. Blackstone ↩︎ ↩︎

-

Google Cloud : $750m partner ecosystem fund. Google Cloud ↩︎